Don’t go all out to boost income without taking account of capital risks.

Let me take you back to the summer of 2018. It was the hottest on record for the UK. Inflation was running at less than 2 per cent, interest rates were at 0.75 per cent, and 18mn people watched Meghan Markle marry Prince Harry and wished them well.

Five years later, inflation is nearly 8 per cent. Interest rates — 5 per cent today — are expected to rise towards 6.5 per cent by the end of this year. And Meghan and Harry? Well, times change.

Although headline inflation is falling — mainly due to fuel prices dropping back to levels from before the invasion of Ukraine — wage inflation seems persistent in the UK. The problem of inflation is not going away quickly. For many investors used to trying to build up their wealth, just preserving its value is now the priority.

Today, several savings firms offer cash products yielding 6 per cent — though often requiring you to lock in for three years. While inflation stays so high, this is costing you nearly 2 per cent a year in purchasing power. At that rate your £1 will be worth around 82p in a decade. Not great, but these returns set a new benchmark for what to expect from other investments.

One area of portfolios worth re-examining is dividend-paying stalwarts. Many high-yielding shares trade on low multiples of earnings and are seen as value stocks. Take National Grid — perhaps the epitome of a solid, steady, low-growth company. It offered a better-than-average yield of 5.5 per cent in 2018. That looked juicy when interest rates were low.

National Grid’s earnings are linked to the assets it employs in electricity networks in the UK and the US, where it has a substantial business. These are rising as it plugs in the ever-growing network of renewables.

Investors should be very careful about assuming that the dividend element they see in the headline data on their investment platform is in the bag — or that share price growth is assured

Simon Edelsten

The growth in earnings has shown in a rising dividend. Between 2018 and 2020 National Grid’s dividend grew from 46p to 49p, keeping up with inflation. From 2020 up to this year’s final dividend the payment should rise to 58p — an increase of 18 per cent. But the cost of living will have risen by about 25 per cent in the same period. The rising cash dividend may feel good, but you are actually getting poorer.

And dividends must be viewed in the context of share prices. National Grid’s share price has risen in five years from around £8 to just over £10. So anyone buying in 2018 did pretty well. But the consequence of that price rise is that the yield is the same now as it was five years ago.

With dividend rises failing to keep pace with inflation, the share price may be vulnerable to a fall to help restore the attractive yield relative to cash. National Grid is not an outlier.

In 2018 the yield on the FTSE 100 was about 4.5 per cent. Today it is the same. Is that enough to compensate you for owning shares rather than leaving money in the bank?

Income managers will remind you that the dividend is only part of the story — an important one. But there is a bit of growth, too, hopefully.

It is a fair point, but investors should be very careful about assuming that the dividend element they see in the headline data on their investment platform is in the bag — or that share price growth is assured.

By way of illustration, potential takeover target BT is down 34 per cent in the past year. It is now delivering a 6 per cent yield, but analysts say rising interest rates mean it needs to cut that dividend drastically to avoid a big rise in its debt costs. If it does, the share price could fall further.

Tear up the textbooks?

Looking across the market, you would normally expect higher interest rates to lead to higher yields in equities. The old-school theory was that value stocks should outperform in times of inflation. Higher inflation leads to higher interest rates and on to higher discount rates. As a result, immediate earnings are worth more to investors than hoped-for cash flow.

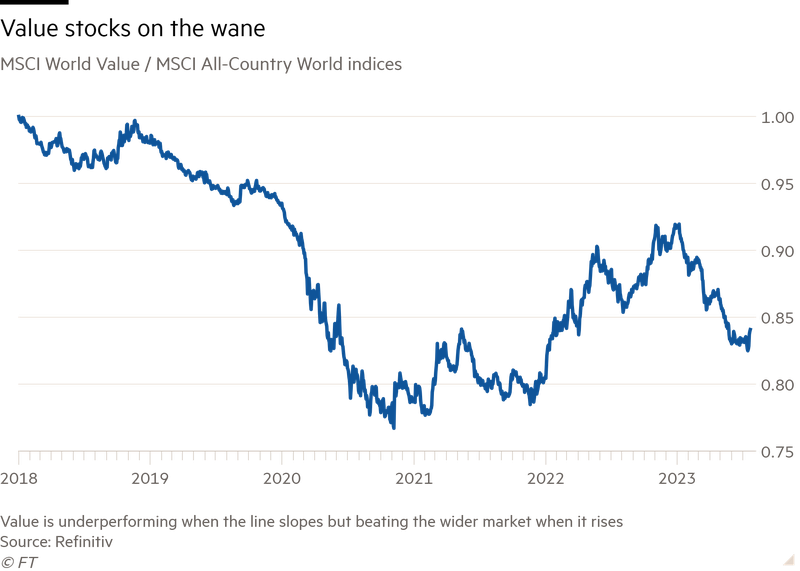

The chart below plots the MSCI World Value Index versus the All-Country World Index (in US dollars). As can be seen, value stocks had a period of outperformance in 2022. But this was largely because the oil stocks in a value basket rose significantly on the invasion of Ukraine. The value index has fallen back this year. So much for the textbooks.

A couple of reasons come to mind. Value-type stocks are often in sectors with poor pricing power (think chemicals), high debts (try utilities and telecoms) and often high labour costs (construction).

The market sees many of today’s growth stocks as a better alternative. Investors believe they are able to outdistance inflation and maintain margin — a slightly exaggerated hope, perhaps, when you see the speed at which Big Tech has been laying off staff lately.

Generally speaking, though, growth stocks that have strong earnings and are reinvesting the bulk of their profits do look more attractive in the face of inflation. That does not mean you should overpay. Some of the share prices in the tech growth sector are now eye-watering. Nvidia could fall 40 per cent but still would not attract new buyers disciplined about cashflow-based valuation.

Is there a middle way?

Well, first it is worth digging below the aggregate numbers. In the US, on average, yields have fallen since 2018. This is largely because of the rise in technology stocks, which often pay no dividends.

But look deeper. Globally, there are still some decent-yielding companies lifting their dividends.

Within the growth arena I would look for stocks on middling ratings that offer some modest yield. Are the cutting-edge stocks priced to perfection really worth so much more? How far would they fall on any failure to keep pace with the hype around them?

There are plenty of steady Eddie stocks that are not that pricey and have long records of maintaining high margins and reinvesting profits wisely. They may not offer the most generous dividends, but they may be better placed to preserve your wealth. Dividends can be important, but be confident they are rising and well covered. Look beyond the headline yield numbers before pressing “buy”.

By Simon Edelsten

© 2023 The Financial Times Ltd. All rights reserved.

This article was legally licensed by AdvisorStream

If you are not currently a subscriber. Click the link below to check out our latest trial offer.